It was a good year for the largest mortgage lender in the nation, despite sticky-high mortgage rates.

United Wholesale Mortgage (UWM), which works exclusively with mortgage brokers, funded a solid $163.4 billion in home loans during 2025.

That was up roughly 17% from their 2024 total of $139.4 billion, likely securing them the top spot for the third year running.

Although, we still have to see what their crosstown rival Rocket Mortgage accomplished during the year (earnings tomorrow!).

What’s interesting though is UWM’s loan volume wasn’t driven by gains in home purchase lending last year.

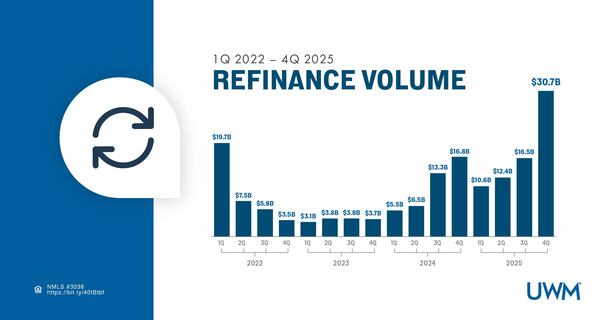

For UWM, It Was All About the Refis Last Year

In recent years, it has been home purchase lending carrying much of the weight for mortgage lenders.

After all, with mortgage rates surging from the 3% range all the way up to 8%, it didn’t make much sense for most existing homeowners to refinance.

A rate and term refinance rarely penciled, and a cash-out refinance was (or should have been) only used in extreme situations where the homeowner was in desperate need of funds.

And so purchase loans allowed the big guys to grow while rates remained high.

That changed last year as seen in United Wholesale Mortgage’s numbers, which became a lot more refinance-heavy.

The lender saw its refinance volume nearly double from $43.4 billion to $70.3 billion, a huge gain given mortgage rates were still above 6% throughout the year.

The fourth quarter was particularly good for refinances, with origination volume s of $30.7 billion, up from $16.5 billion in the third quarter and $16.8 billion in the fourth quarter of 2024.

According to UWM, it was their best refinance year since 2021. And we all remember how good refinances were back then, the year the 30-year fixed hit an all-time low.

Purchase Lending Actually Slowed During the Year

That brings me to home purchase lending. While refinances were hot last year, and could be even hotter this year, purchase lending cooled at UWM.

The company said it funded only $93.2 billion in purchase loans during 2025, compared to $96.1 billion the year prior.

It wasn’t a big drop, but it was a drop. And that’s not a great sign for the housing market, which has struggled mightily of late.

Long story short, housing affordability has been really poor and you’re seeing it in the numbers from top lenders like UWM.

While existing homeowners have been able to get mortgage payment relief, we aren’t seeing new buyers jump into the market.

Recent numbers were even less encouraging, with purchase originations of just $18.9 billion in the fourth quarter compared to $25.2 billion in the third quarter.

That was also down from $21.9 billion in the fourth quarter of 2024.

Will Sub-6% Mortgage Rates Change Things for 2026?

The big question now is what will 2026 look like for the biggest mortgage lenders in the industry?

Mortgage rates finally fell into the 5s this week and if they can stay there for a reasonable amount of time (or all year!), we could see purchase lending pick up.

But the fact that it’s been mostly a refinance party with lower rates tells you there’s a real chance home buyers might not bite. Or won’t bite as much as expected.

Sure, it’s cheaper than it was last year (and probably the year before that), but it’s still expensive to buy a home today.

And ultimately a rate of 5.875% versus 6% isn’t much different in terms of math. We’re talking $30 on a $400,000 loan.

However, if buyers can afford it and the sentiment improves with lower mortgage rates, we might see both purchase lending and refinance lending increase in 2026.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.