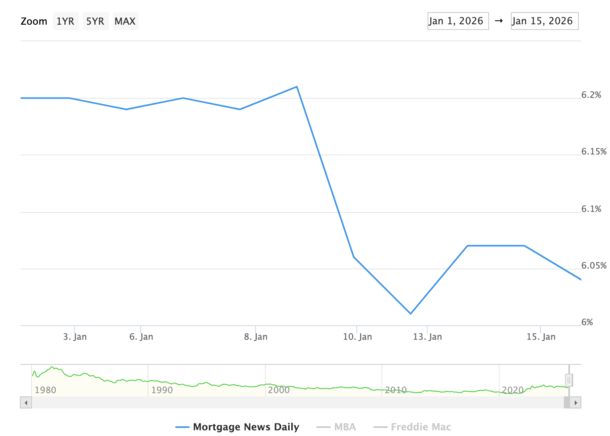

At last glance, the 30-year fixed was back in the 6% range, rising from a brief spell in the 5s after news broke that Fannie and Freddie would buy mortgage-backed securities (MBS).

Trump’s plan for the pair to buy $200 billion in MBS sent mortgage rates down last Friday to sub-6% levels.

But the initial 5.99% reading at Mortgage News Daily was short-lived, and rates ended the day with a midday reprice of 6.06%.

They opened Monday at 6.01%, before bouncing to 6.07% midweek, and then falling back to 6.04%.

So while they aren’t in the 5s quite yet, at least when we consider the national average, they sure are close.

Mortgage Rates Struggle to Break Through to the 5% Range

While it appeared as if we were finally into the 5s last Friday, it proved to be elusive as a reprice sent rates back to 6.06%, per MND.

The initial reaction to the $200 billion MBS buying program was cheered by mortgage lenders, loan officers, and mortgage brokers alike, but then we saw a pullback.

The 30-year fixed fell from 6.21% last Thursday to 5.99%, a big one-day move of nearly 0.25%, before bouncing and ending the day a little higher.

It then closed the following Monday at 6.01%, but again, not quite the 5.99% reading everyone so desperately wanted.

Despite this, the national headlines ran with the 5.99% reading that was in play briefly and didn’t look back.

Clearly it sounds a lot better to say mortgage rates are in the 5s than it does saying 6.01%.

I always thought it was interesting that MND essentially chose 5.99% as their rate that day since there’s some level of subjectively in the rate index.

Had they said 6.06% initially, the reaction would have been far more muted, despite the difference in payment being negligible.

But it does kind of point to resistance at the 6% threshold.

Lenders Always Price Mortgage Rates Defensively!

This is a good reminder that mortgage lenders always price defensively.

The best way to illustrate this is they are quick to increase mortgage rates if we receive bad mortgage rate news.

Conversely, if we get good mortgage rate news, they’ll take their sweet time lowering rates.

After all, they won’t want to get caught off-guard and be priced below market and lose their tails. MBS investors also need time to re-calibrate.

However, they still did lower their rates with many offering a 30-year fixed an .125% or a .25% below levels the day prior.

So they didn’t sit on their hands, but given the news was kind of out of nowhere, they probably didn’t extend the full discount either.

They need the dust to settle to see how it’ll all work, the timeline, and maybe just the assurance it’s actually going to happen.

For the record, Fannie and Freddie were already upping their purchases of MBS before this news broke, but without any fanfare.

This is a much bigger buy, assuming it happens, so it was more impactful.

How Much Lower Can Mortgage Rates Get?

Now the question is if/when this program gets underway, will mortgage rates drop even more?

Or is it mostly baked in already given rates are still hovering close to 6%, which is far below the 6.21% we saw prior the announcement?

One could make the reasonable argument that about half the discount is already priced in, and another half could be coming.

So if the 30-year fixed by MND’s measure dropped about 15 basis points, we could see another 15 bps in improvement.

Give or take a basis point, perhaps that gets us to 5.875%. It’s not a massive payment difference, but it would be a big psychological win for the housing market.

It’d be heralded as big news and undoubtedly touted by the White House as a major victory for home buyers.

Just note that the MBS buying is just one component of mortgage rate pricing.

We still have to pay attention to what’s going on in the wider economy, with inflation and labor still major factors that drive rates.

If that data isn’t favorable, it could offset the benefit of the MBS buying. Of course, if the data is interest rate-friendly, rates could be pushed further into the 5s…

Read on: 2026 Mortgage Rate Predictions

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.