1. Mortgage rates will fall into the 5% range

2. Home prices will be flat (if not lower)

3. Affordability will improve but remain constrained

4. Home sales will rise, but not as much as expected

5. The home builders will struggle to move inventory

6. More borrowers will turn to adjustable-rate mortgages

7. The biggest mortgage lenders will gain market share

8. More homeowners will tap equity to maintain lifestyles

9. We’ll see short sales make a return

10. The housing market won’t crash

Bonus: We’ll see some sort of new housing policy rolled out by the Trump Administration.

2025 Was a Little Better Than 2024

Welp, another year has come and gone, and while it wasn’t much different than 2024, things were a little brighter for the mortgage and real estate industry.

If you recall, the saying in 2024 was “survive ‘til ’25.” There doesn’t seem to be a similar slogan for 2026 so perhaps the worst is behind us.

Sure, some still think we are on the cusp of another housing crash, but when you dig into the details, all the ingredients simply aren’t there.

Instead, chances are it’ll be a little more of the same in 2026, though with conditions slowly returning to normal.

Of course, real estate is local so performance will always vary by market.

Mortgage Rates Will Fall Into the 5% Range

I always start with mortgage rates because that’s always the most talked about topic.

My general thinking is mortgage rates will finally dip into the 5s in 2026, likely by the first quarter.

I get that there’s resistance at those levels, but we’re also only about 20 basis points away.

Ultimately, it will only take a bad jobs report or two to get us there, assuming inflation continues to show signs of improvement.

The monthly savings might not be huge, but it would be enough to get more rate and term refinances to pencil.

And it would be a psychological victory for prospective home buyers from a sentiment standpoint.

You can see all the 2026 mortgage rate predictions in the associated post to see what others think. The quick takeaway is mostly flat.

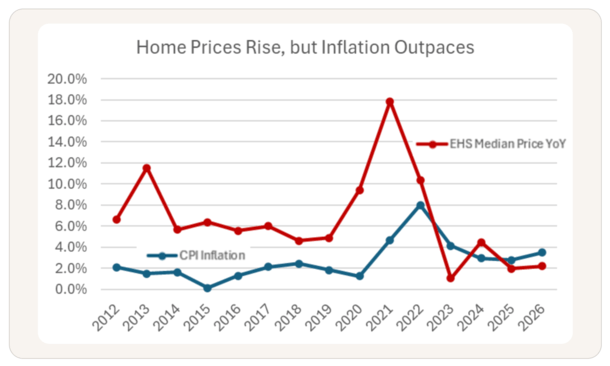

Home Prices Will Be Flat (or Even Lower)

Just as most pundits expect flat mortgage rates in 2026, most expect home prices to be relatively unchanged as well.

The forecasts vary somewhat, but Zillow only expects a 1.2% rise in property values next year.

And it’s an even lower 0.5% increase from Compass chief economist Mike Simonsen.

Over at Realtor, they expect a 2.2% increase, which is still pretty flat, and not much better than the 2.2% seen this year.

That means real home prices, adjusted for inflation, would be down, even if they’re up on a nominal basis.

In some markets, such as the hard-hit Sun Belt, home prices could actually fall on a nominal basis.

I don’t expect big declines, but it’s certainly possible to see negative YoY changes given rising inventory and poor affordability.

Affordability Will Improve But Not Enough

Speaking of housing affordability, the combination of lower mortgage rates and flat (or lower) home prices will be a positive for prospective home buyers.

The problem is it’s likely not going to be enough to really move the dial. We’ve seen affordability slowly improve this year for these same reasons.

And it’ll likely continue into 2026, but might not be enough to get a borrower’s DTI ratio in range. Or simply entice them to jump off the fence.

At the same time, it may not sway someone to list their home, knowing they’ll need to purchase a replacement property.

We’ve had a lot of would-be sellers dominate the market in recent years, and we also have would-be buyers too.

It’s a standoff that has slowly gotten better, but continues to be fester because not a whole lot has changed.

Home Sales Will Rise, But Fall Short of Expectations

I do believe home sales will rise in 2026, but from very low levels. Remember, existing home sales were at a near-30 year low in 2024, just above four million.

This year they rose marginally and next year they’re expected to inch up further, but remain close to four million.

Fannie Mae pegs the existing sales rate at about 4.4 million, which is a decent 7.5% improvement, but well below what NAR expects.

More of the same problems will plague the housing market in 2026, including poor affordability, mortgage rate lock-in, and limited for-sale inventory.

It could be a lot worse, but it’s not going to be a bonanza, even with mortgage rates potentially falling below 6%.

Especially if the economy takes a turn as consumer spending finally catches up to us, and job losses mount.

The Home Builders Will Struggle

The past few years the home builders were on a roll because they were kind of the only game in town.

Nobody was listing their homes, so they had little competition, despite poor home buyer demand.

In addition, they were able to buy down mortgage rates significantly using a special advantage known as a forward commitment.

This meant mortgage rate buydowns into the 2s and 3s (or even lower), enough to entice skittish buyers to take the plunge.

However, they’ve seen their inventory begin to pile up as sales have slowed, with transactions expected to fall 1.6% this year, per Fannie Mae.

They do expect a 4.5% uptick in new home sales in 2026, but I’m not fully convinced given the locations of new homes are in areas with a supply glut.

And even with big sales concessions, the builders are struggling to move homes.

The one caveat is if they get some sort of boost from a new policy change, or some sort of subsidy push.

More Borrowers Will Rely on ARMs

Lately, there’s been a shift to adjustable-rate mortgages, which have come down with short-term rates like the federal funds rate.

With the expectation that the 30-year fixed may have peaked and could be flat, some are choosing an ARM to achieve an even lower payment.

It can make sense if the interest rate spread is favorable, though you have to be careful because some lenders barely offer a discount versus a 30-year fixed.

We’ve also seen the home builders turn to ARMs instead of fixed-rate mortgages because it’s cheaper for them to drive down the monthly payment for their customers.

Again, understand what you’re getting isn’t as good as a 30-year fixed. Though today most ARMs are fixed for 5-7 years or longer, such as the 5/6 ARM and 7/6 ARM.

That’s a lot of time to hope for even lower rates in the future and in the meantime, pay less and pay down the loan faster (due to the lower rate).

The Biggest Mortgage Lenders Will Get Even Bigger

The story of 2025 was mortgage lenders acquiring real estate companies and loan servicers, all in an effort to grow even larger.

We saw Rocket acquire both real estate brokerage Redfin and major loan servicer Mr. Cooper.

And the nation’s top lender, United Wholesale Mortgage, acquire Two Harbors, another larger loan servicer.

Then there was Lower, which scooped up real estate portal Movoto and later partnering with real estate brokerage HomeSmart.

In addition, Compass acquired rival brokerage Anywhere Real Estate and that could benefit the preferred lender Guaranteed Rate.

I expect more of these sorts of deals to happen in 2026 and for the closed ones to begin to bear fruit.

This coincides with the new trigger law rule, which requires lenders to have permission to reach out to borrowers (or a prior relationship).

Guess who will have a prior relationship? Yep, the big guys who own all these other companies and/or service the existing loans.

That gives them more recapture opportunities while simultaneously shutting out their competitors.

This is good for the big guys, but may hurt consumers if there’s less lender choice.

More Homeowners Will Tap Their Equity to Keep Spending

We already saw home equity lending rise quite a bit the past couple years, but it still pales in comparison to the early 2000s.

In addition, there are very few cash-out refinances these days, so most equity extraction is only coming via second mortgages like HELOCs and home equity loans.

As such, the numbers, while higher, aren’t all that crazy. I’ve said for a while that if and when homeowners really go nuts tapping equity, we could run into problems again.

Especially if home prices fall and/or if lenders get more liberal with maximum CLTVs.

The problem these days is many homeowners need to tap equity just to keep up with their spending, which is a bad sign for the wider economy.

While that sounds frightening, lending standards today are still way better than they were in the early 2000s.

And as noted, most homeowners are keeping their low-rate, fixed first mortgages intact because they’re so cheap.

The Return of the Short Sale

I’ve been hearing more and more rumblings of short sales return to the housing market.

This is when property owners are underwater on their mortgages (owe more than the property is worth) but still need to sell.

They were very common during 2008-2013, but have been virtually non-existent since then as home prices surged and mortgage rates hit record lows.

But we’re now at a tipping point again with home prices falling in some markets, notably places like Florida and Texas.

Those who took out 3%-down mortgages who have seen their property fall in value could be in trouble if they NEED to sell.

This is especially pertinent for the recent vintages of home buyers, think late 2022 and 2023, when mortgage rates were also high.

Very little of the loan balance has been paid off and when combined with a flat/lower sales price and transaction costs, it could be short sale territory.

To that end, we might also see an uptick in foreclosures as loss mitigation options begin to tighten up as well.

But again, the good news is the vast majority of homeowners either own their homes free and clear, or have a mortgage rate in the 2-4% range.

The Housing Market Won’t Crash in 2026

Something I’ve pointed out a few times is that most of today’s mortgages were originated when rates hit record lows.

This was in early 2021, and since then, home prices have also surged higher. This means your typical homeowner has a super low rate, a small loan balance, and a low LTV ratio.

Yes, recent home buyers are in the exact opposite position, having bought at the height of the market with 6-8% mortgage rates.

But here’s an important detail. Home sales fell off a cliff when affordability tanked, as we’ve seen with the transaction numbers hitting those 30-year lows.

While it’s been hard on the industry, whether it’s real estate agents or loan officers and mortgage brokers seeing fewer transactions, it’s good for the market.

It’s a healthy response for sales to slow if conditions warrant it. In the early 2000s, we forced sales through with highly-questionable financing, which is generally what causes bubbles.

Thanks to the ATR/QM rule, we just haven’t seen the same level of high-risk lending this cycle, even if FHA loans are a weak spot.

Like I said, the housing market won’t be free of distressed sales in 2026, but it won’t be anything like GFC conditions.

It’s actually normal to have distressed sales and not an outright bull run every year.

Will the Trump Admin Finally Deliver Housing Policy Change?

One last bonus prediction. I believe the Trump admin will come through with some sort of policy change in 2026.

Granted, this isn’t a bold prediction because Trump himself said the other day that he would “announce some of the most aggressive housing reform plans in American history.”

So he better show up with something halfway decent. Of course, he pinned the blame of high home prices on illegal migration in that same speech.

Meanwhile, they really went up because of record low mortgage rates combined with low levels of home building post-GFC.

But given his admin has already floated all types of wild ideas, such as the 50-year mortgage, portable mortgage, and making more mortgages assumable, which all fell flat, it’ll likely be something less exciting.

Perhaps deregulation for home builders to build faster and cheaper. Of course, new builds aren’t the be all, end all solution, especially since their inventory is already piling up.

Expecting the home builders to build more when they can’t even move existing inventory would be silly.

Though if there were some subsidies for buyers, it could potentially help. They just have to be mindful of balancing supply and demand, and not just making the market hot again.

In the meantime, we’ll continue to wait for the promise he made during his campaign to bring mortgage rates back down to 3% or even lower!

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.