Welp, just like that it appears mortgage rates are moving back down toward 6.50%, possibly lower.

And you can thank a super weak labor market for that, something many whispered about though it was never justified in the data.

That may have finally changed this morning, with an ultra-soft jobs print reported for July, and even bigger downward revisions for the months of June and May.

Now the labor market isn’t looking so hot, a development that could force the Fed to resume cutting.

Bond yields were a lot lower on the news, which means mortgage rates will also come down significantly.

The Labor Market Breaking Is Great News for Mortgage Rates

It’s an awkward situation, at least for prospective home buyers, existing homeowners, and those working in mortgage and real estate.

The labor market all of a sudden looks very shaky, and while that’s bad news for just about everything else, it could be at least bittersweet news for the housing market.

You see, when the economy shows signs of weakness, mortgage rates tend to move lower.

And the labor market and wider economy has proven resilient month after month, making it difficult for interest rates to come down.

So much so that the Trump administration has attacked Fed Chair Jerome Powell repeatedly to lower rates.

But Powell was steadfast, arguing that inflation could worsen due to tariffs, while noting that employment was still holding up.

In fact, in its July FOMC statement, the Fed said, “the unemployment rate remains low, and labor market conditions remain solid.”

That was uttered just two days ago, when the Fed held rates steady, much to the chagrin of President Trump and FHFA director Bill Pulte.

Now it might not appear to be so solid. Why? Well, for starters the July job numbers came in well short of expectations.

Just 73,000 jobs were added last month, below the forecast of 100,000 jobs. A low estimate to begin with, and an even lower figure reported.

But that was just the tip of the iceberg. The U.S. Bureau of Labor Statistics (BLS) also revised down the numbers from both June and May.

And it was ugly. Or whatever is beyond ugly. For June, they revised the jobs added from 147,000 to just 14,000. That was a 133,000 haircut.

It was nearly the same story for May. Jobs were revised down by 125,000 from 144,000 originally reported to just 19,000 added.

Taken together, just 106,000 jobs were added over the past three months! That’s barely above the estimate for just July!

And who knows if the July numbers will even stand. Will those be revised down later too?

Has the labor market finally cracked? It certainly looks like it might have.

Ironically, Federal Reserve Vice Chair Michelle W. Bowman warned this morning “a delay in taking action could result in a deterioration in the labor market and a further slowing in economic growth.”

Fed Rate Cuts Back on the Table for 2025?

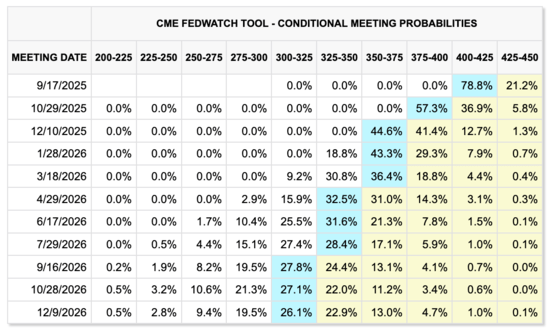

Yesterday, the odds of a Fed rate cut in September were just 37.7%. Today, those odds climbed to a staggering 78.7%, per CME.

In other words, expect a Fed rate cut in two months. And perhaps another in October and another in December, per the chart above.

Just like that, the three rate cuts expected for 2025 are back. Prior this jobs report, there was just one rate cut expected for 2025.

While Fed rate cuts don’t directly correspond to lower mortgage rates, nor does the Fed control mortgage rates, they take cues from economic data.

As noted, weak economic data is good for mortgage rates, so they will likely move a lot lower today.

And if we continue to see weak economic data in the months ahead, mortgage rates will continue lower from there.

This could mean that 30-year fixed mortgage rates fall to the low-6% range by year-end (or even lower), as many mortgage rate predictions for 2025 originally projected.

I went out on a limb late last year and said the 30-year fixed could be 5.875% at some point in the fourth quarter of 2025.

While that sounded crazy as of yesterday, it’s firmly back on the table today. Of course, at the expense of perhaps the economy!

But this is a good reminder not to call it too quickly. I’ve been saying for a while that there was lots of time left in 2025.

Still five months to go since it’s only August 1st. A lot can still happen so I wouldn’t rule anything out.

Just remember that mortgage rates can be erratic, and it’s never a straight line up or down.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.