It’s no secret certain folks don’t like Fed Chair Powell. You may have heard of one of them, President Donald Trump, who refers to him as a “Too Late Powell.”

He also calls him other names that I won’t repeat here.

Now he’s got another strong critic in FHFA Director Bill Pulte, whose agency oversees Fannie Mae and Freddie Mac.

These two companies are responsible for most of the mortgages in existence, with conforming loans far and away the most common loan type out there.

For this reason, Pulte has called on Powell to lower rates or resign, the strongest words he’s uttered since taking the helm at the FHFA.

Cut Rates or Resign Powell

Pulte went off in a series of posts on X, saying very directly, “I am calling for Federal Reserve Chairman, Jay Powell, to resign.”

He followed that tweet with more one-liners, including, “There is no legitimate factual basis to keep rates high. None.”

And this one: “Americans are sick and tired of Jerome Powell. Let’s move on!”

But he was just getting started. He went on to write, “…he is hurting Americans and hurting the mortgage market, which I am responsible for regulating.”

Then explained how Powell is “the main reason” we have a so-called housing supply crisis in our country.

That “by improperly keeping interest rates high,” Powell has trapped homeowners in low-rate mortgages while choking off for-sale supply.

He ended that tweet by repeating that “He must lower rates.”

So it’s pretty clear Pulte, like Trump, isn’t a fan of Powell. That’s fine. Everyone has a right to their own opinion.

And perhaps interest rates should be lower today. But it should be noted that the Fed doesn’t control mortgage rates.

They control their own policy rate, the short-term fed funds rate, which doesn’t have a clear relationship with the 30-year fixed over time.

Meaning if Powell were to cut the Fed rate tomorrow, or a couple days ago at their meeting, the 30-year fixed wouldn’t necessarily respond in any expected way.

In fact, the 30-year fixed could be higher as a result. If you recall back in September when the Fed cut rates, mortgage rates increased.

I wrote about that already, and the takeaway is that it’s a complicated relationship.

We Can’t Bully Our Way to Lower Mortgage Rates

At the end of the day, we can’t force mortgage rates lower by yelling at Powell and the other Fed members to lower rates.

They don’t control long-term rates like the 30-year fixed. Not sure how many times that needs to be said, but it’s getting tiresome.

The only way they can actually, directly lower mortgage rates is via another round of Quantitative Easing (QE), where the Fed buys Treasuries and residential mortgage-backed securities (MBS).

This was how mortgage rates hit record lows in 2021 in the first place, and also why we’re in this mess today.

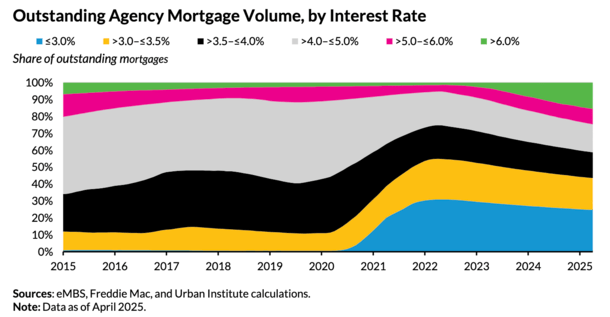

To Pulte’s point about homeowners being trapped in low-rate mortgages, that’s a phenomenon known as the mortgage rate lock-in effect.

It’s the result of homeowners taking out 2-4% fixed-rate mortgages and now facing rates closer to 7%.

The big gap in rates (see chart above from the Urban Institute) makes it less compelling to move, and thus homeowners stay put, which further exacerbates the existing housing supply shortage.

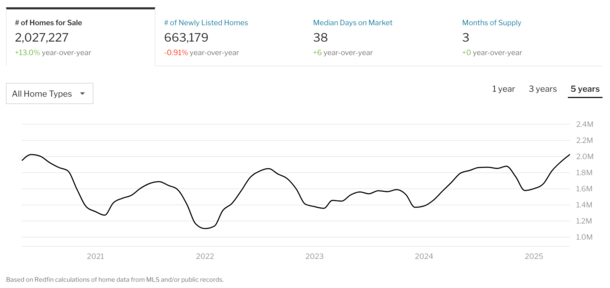

Housing Supply Is Finally Growing and Up 13% From a Year Ago

However, supply is growing rapidly and at last glance, is up 13% from a year ago, per Redfin.

And it’s finally getting back to pre-pandemic levels, when home buyers scrambled to take advantage of the lowest mortgage rate in history, depleting supply in the process.

So we’re moving in the right direction in part because of higher mortgage rates, which have cooled demand and led to better equilibrium between buyer and seller.

Cutting rates just to boost affordability might not allow that process to continue. And as noted, that’s not how it works anyway.

The underlying economic data needs to support rate cuts, which would also drive bond yields lower (and by extension mortgage rates too) before a Fed rate cut.

It’s a process that takes time and it’s playing out. We just need to be patient and we’ll get there, while also creating a sustainable path to affordability.

The housing market doesn’t need rock-bottom mortgage rates again. It needs normalcy. And if we’re patient, that’ll come.

If we manipulate the market (how we got in this mess to begin with), yet again, as we did with multiple rounds of QE, we’ll just create bigger problems and continue to kick the can.

(photo: iandesign)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.