Welp, the question I asked recently, would mortgage rates hit 5.99% or 7% next, has been answered.

And unfortunately, if you’re a prospective home buyer or recent homeowner looking for rate relief, it’s 7%.

The latest foe for mortgage rates is a new round of global tariffs, including a whopping 104% tariff on Chinese imports.

That was enough to rattle the bond market, which drives the prices of mortgage rates.

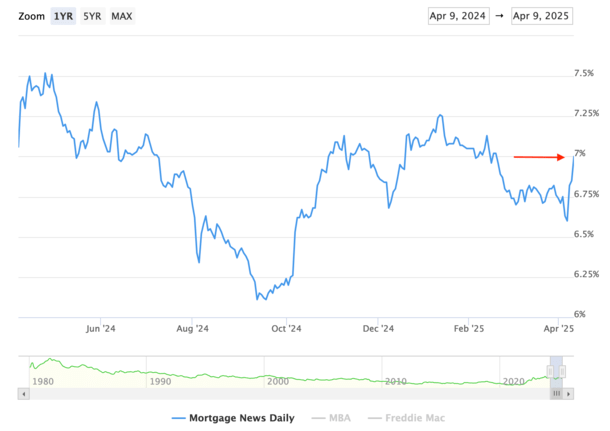

As a result, the 30-year fixed is now priced exactly at 7%, per Mortgage News Daily.

7% Mortgage Rates Are Back

Just when you thought they were gone forever, high mortgage rates they’re back. The 30-year fixed is at an even 7% today, up from 6.85% yesterday, per MND.

That’s a big one-day move, and it came on the heels of another big one-day move on Monday when rates jumped 22 basis points (0.22%).

We’ve now gone from 6.55% at the end of last week to 7%, which is pretty astonishing.

As noted, the driver is the new round of tariffs, which is a sky-high 104% on China, including a “previously imposed 20% duty, a 34% additional tariff and a last-minute 50% increase that Trump signed late Tuesday.”

China responded immediately, raising its tariff on U.S. goods to 84% from a previously announced 34%.

The European Union (EU) also approved retaliatory tariffs on U.S. imports, which will go into effect on April 15th.

In other words, we are in a full-scale global trade war. There is no bluffing, there is no negotiating (thus far), and maybe even no going back to the status quo.

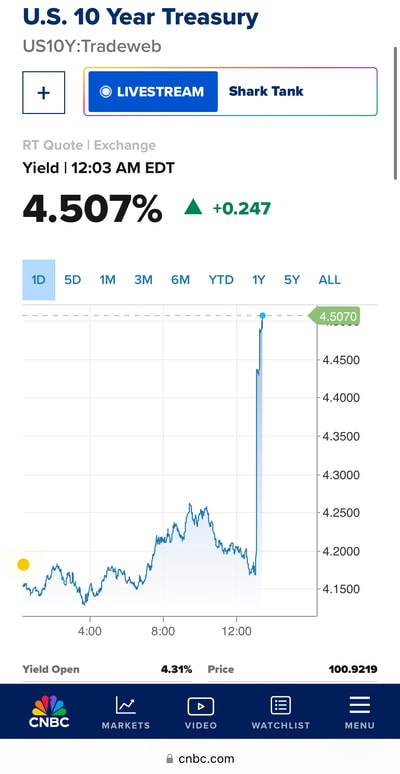

The immediate effect was bond yields skyrocketing in the overnight session to above 4.50%, before settling in around 4.35% as of this writing.

Combined with a mortgage rate spread that has also widened as a result of the volatility, the 30-year fixed is back above 7%.

Over at Wells Fargo, which I also track, the 30-year fixed was priced at 6.875%, up from 6.25% as recently as Friday.

If this keeps up, they too might need to exchange the 6 with a 7, despite the psychological message it will send to customers.

Mortgage Rates Are Rising Just in Time for Spring Home Buying

The worst part is that this couldn’t come at a worse time for the housing market, which was already showing signs of weakness.

Rising for-sale inventory, stale listings, price drops, and poor affordability will now be accompanied by 7-handle mortgage rates.

Not exactly ideal when home builders are trying to move their growing inventory, and prospective home buyers are simply trying to make a deal pencil.

Same goes for sellers, who were hoping lower mortgage rates could massage the transaction, in spite of the worst affordability in recent history.

What’s interesting though is that mortgage rates are historically bad in the months of April and May.

So this is actually very on brand for mortgage rates. They’re behaving as the normally do.

The problem is the speed and magnitude of change. If rates had kind of just stumbled along in the high 6s and low 7s all year, nobody would be too upset.

But they were dropping before this massive reversal, looking like they were making a move toward the high-5s.

Then boom, it’s back to 7%. I said a while back that I didn’t know if the housing market could stomach 7% mortgage rates again.

Sure, it’s not a huge difference in monthly payment, going from say 6.75% to 7%, but the mental cost is unknowable.

If you’ve been house hunting for the past year and paying attention to the lower rates on offer, only to see them jump back past 7%, it’s another gut-punch that could be the final straw.

What Happens Next with Mortgage Rates?

Ah, the million-dollar question. Is this the start of something really bad, or just some short-term noise we’ll forget about in a month?

It’s hard to say. On the one hand, it feels like a paradigm shift, like we’re completely upending the status quo on global trade.

On the other, it could be some really intense theater mixed with some next-level negotiating.

Whatever it is, the markets don’t like it, whether it’s the stock market or the bond market.

Both have sold off at the same time, while recession odds are rising by the minute (now around 60%).

It should be pointed out that the 30-year fixed was around 7.50% in April 2024. So today’s mortgage rates remain quite a bit lower.

And the Fed is now expected to cut its short-term fed funds rate four times this year, up from just one or two recently.

This will at least be good for HELOC rates, which are tied to the prime rate that moves in lockstep with the FFF.

Whether long-term bond yields follow suit is another question, but I wouldn’t be shocked if rates settled back down in the third quarter.

In my 2025 mortgage rate predictions post, I actually said rates would be lower in the first quarter than the second quarter, before going even lower in the third and fourth quarter.

So far that’s going to plan. Perhaps we’ll just need to weather a few bad months before the rate relief comes later in the year.

Problem is we risk yet another terrible spring home buying season, which could result in falling home prices and possibly more distressed sales.

The good news is most homeowners have fixed-rate mortgages set at 2-4%, so they’ll have a really good incentive to hang onto them.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.